TAX & COMPLIANCE · FOR SME OWNERS

Australian small business tax has a reputation for being complicated. It mostly isn’t. There are five core taxes most SMEs deal with – GST, PAYG instalments, PAYG withholding, fringe benefits tax, and superannuation guarantee – and once you understand the rhythm of each, the year becomes predictable.

This handbook walks through all five in plain English, with 2025-26 thresholds, the due dates that actually matter, and the mistakes that catch most owners off-guard.

The four rhythms of Australian SME tax

Every Australian small business eventually settles into four annual rhythms:

- Quarterly BAS: due 28th of October, February, April, and July. Reports GST, PAYG instalments, and PAYG withholding for the previous quarter.

- Monthly super: due 28th of each month following the quarter (so 28 October for Jul-Sep), with payday-super reforms expected from 1 July 2026.

- Annual tax return: due 31 October if you self-lodge, later if you use a registered tax agent.

- One-off events: FBT year-end (31 March), end of financial year (30 June), Single Touch Payroll reporting.

Get those four rhythms running on autopilot – set up calendar reminders, use accounting software that prompts you, hand a checklist to your tax agent – and Australian tax stops being a fire drill.

GST (Goods and Services Tax)

GST is a 10% tax on most goods and services sold in Australia. As a business, you collect GST from customers, pay GST on your business inputs, and remit the difference to the ATO via your BAS.

When you have to register

You must register for GST if your business turnover is $75,000 or more in any rolling 12-month period (not just a financial year), if you’re a ride-share or taxi driver (regardless of turnover), or if you want to claim fuel tax credits. You can register voluntarily below $75,000 if you want to claim GST credits on inputs – useful for businesses with significant start-up costs.

How it works

When you sell something for $110, $10 of that is GST you owe to the ATO. When you buy something for $55, $5 of that is GST you can claim back. Your BAS sums these up – output tax minus input tax credits – and you pay or receive the difference each quarter.

Common mistakes

- Charging GST before you’re registered (illegal – you can’t charge it until your ABN is GST-registered)

- Treating BAS due dates as suggestions (late penalties start at $313 and escalate)

- Forgetting GST on insurance, council rates, and small one-off purchases

BAS (Business Activity Statement)

The BAS is the quarterly report covering GST, PAYG instalments, PAYG withholding, fuel tax credits, and other items.

Quarterly due dates

- Q1 (Jul-Sep): due 28 October

- Q2 (Oct-Dec): due 28 February

- Q3 (Jan-Mar): due 28 April

- Q4 (Apr-Jun): due 28 July

Using a registered BAS agent typically gives you a four-week extension. Worth the fee.

Practical tip

Set up a separate bank account just for tax. Each time GST is collected on a sale, move 10% across automatically. When BAS time comes, the money is already there.

PAYG: two different things with the same name

PAYG instalments are your income tax, paid quarterly in advance based on your previous year’s earnings. PAYG withholding is the tax you deduct from your employees’ wages and remit to the ATO. When someone says “PAYG”, ask which one they mean.

Superannuation Guarantee

If you employ anyone (including yourself if you pay yourself a salary from a Pty Ltd), you must pay superannuation guarantee on top of their wages. The 2025-26 rate is 12% of ordinary time earnings.

Why missing super payments is the worst tax mistake

The ATO treats unpaid super differently from other tax debts. You lose the tax deduction, pay interest, pay administrative penalties, and risk director’s penalty notices recovering the debt personally – even if your company is the legal employer. Unpaid super is one of the few business debts that can pierce the Pty Ltd liability firewall. Pay super first, before anything else.

FBT (Fringe Benefits Tax)

FBT is the tax on non-cash benefits employers provide to employees, paid by the employer at 47%. Common fringe benefits: company car for private use, entertainment above the minor-benefits threshold, below-market loans, payment of personal expenses.

For most small businesses, FBT is best avoided rather than managed. Structure car use as expense reimbursement; keep client lunches under $300 minor-benefit threshold; pay yourself a salary rather than paying personal expenses through the business. Talk to your tax agent before providing any non-cash benefits.

Single Touch Payroll (STP)

If you employ anyone, you must report wages, tax, and super via STP each pay run. STP Phase 2 requires more detail. Every modern payroll system (Xero, MYOB, KeyPay, Employment Hero) handles STP automatically.

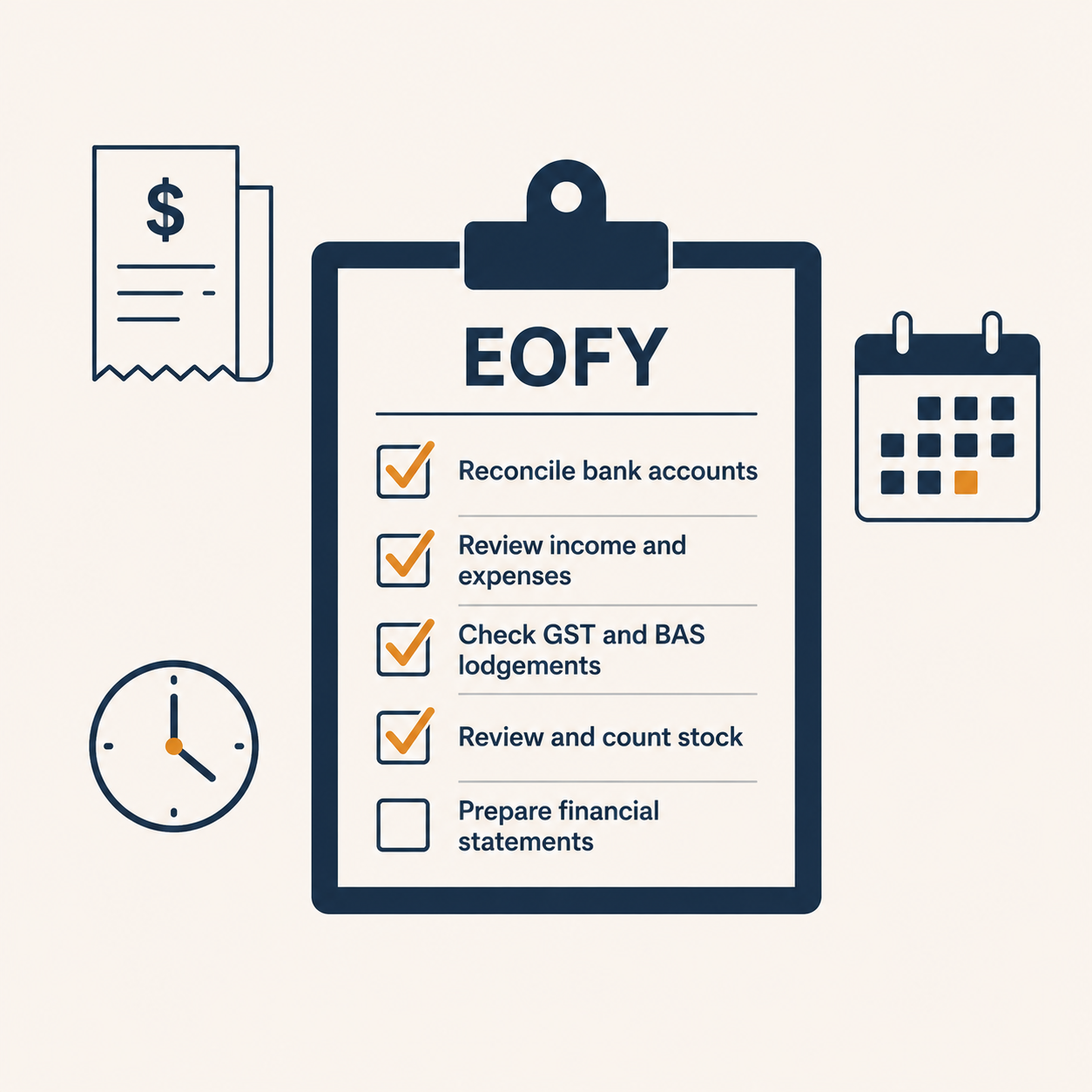

End-of-financial-year checklist

- Stocktake if you carry inventory

- Write-off bad debts before 30 June to claim them this year

- Pay super for the June quarter by 28 July (earlier if going for deduction this year)

- Document home-office, vehicle, or asset use percentages

- Instant asset write-off: claim eligible assets purchased before 30 June

- Trustee resolution (if you run a trust) – document distribution decisions in writing

- Schedule tax-planning meeting with your agent in May, not late June

Plain-English Australian tax in your inbox each week

For SMEs, tradies, and founders. Free, forever.

Frequently asked questions

How often do I need to do a BAS?

For most small businesses: quarterly. Smaller businesses (turnover under $20M) can elect annual GST returns. Larger businesses report monthly.

What’s the difference between PAYG instalments and PAYG withholding?

PAYG instalments are your own income tax paid quarterly in advance. PAYG withholding is the tax you deduct from your employees’ wages.

Do I have to pay myself super as a sole trader?

No. Sole traders aren’t required to pay themselves super guarantee. Many make voluntary contributions for tax efficiency. From a Pty Ltd paying yourself a salary, super guarantee applies.

What happens if I’m late paying super?

Significant penalties: lost deduction, interest, administrative penalties, risk of director’s penalty notices. Pay super on time, every time.

Sources

- ATO – GST registration: ato.gov.au/businesses-and-organisations/gst

- ATO – BAS lodgement: ato.gov.au/businesses-and-organisations/business-activity-statements

- ATO – Super guarantee: ato.gov.au/business/super-for-employers

- ATO – FBT: ato.gov.au/business/fringe-benefits-tax

Disclaimer: General educational information based on Australian tax law as at May 2026. Rules and thresholds change frequently. Verify current rates with the ATO before making decisions. Not a substitute for advice from a registered tax agent.