FOR ESTABLISHED BUSINESSES

Profitable businesses fail because of cash flow, not profit. Roughly four in five Australian small-business closures involve cash-flow problems, not absent profitability. You can run a business that’s making money on paper and still go broke. This article is about the disciplines that make sure that doesn’t happen to you.

Why profit and cash flow are not the same thing

Profit is what your accountant reports after a quarter. Cash is what’s in your bank account on a Tuesday. The two are related but not the same:

- A customer might owe you $50,000 in unpaid invoices (counted as revenue) while you’re $5,000 short on payroll on Friday.

- A $30,000 vehicle purchase shows up as $8,000 of depreciation expense over the year but takes $30,000 out of your bank on day one.

- GST collected on sales sits in your account for three months before going to the ATO – looking like cash you have, when it isn’t yours.

Most owners only learn these distinctions when cash runs out. The whole point of forecasting is to learn them before the squeeze.

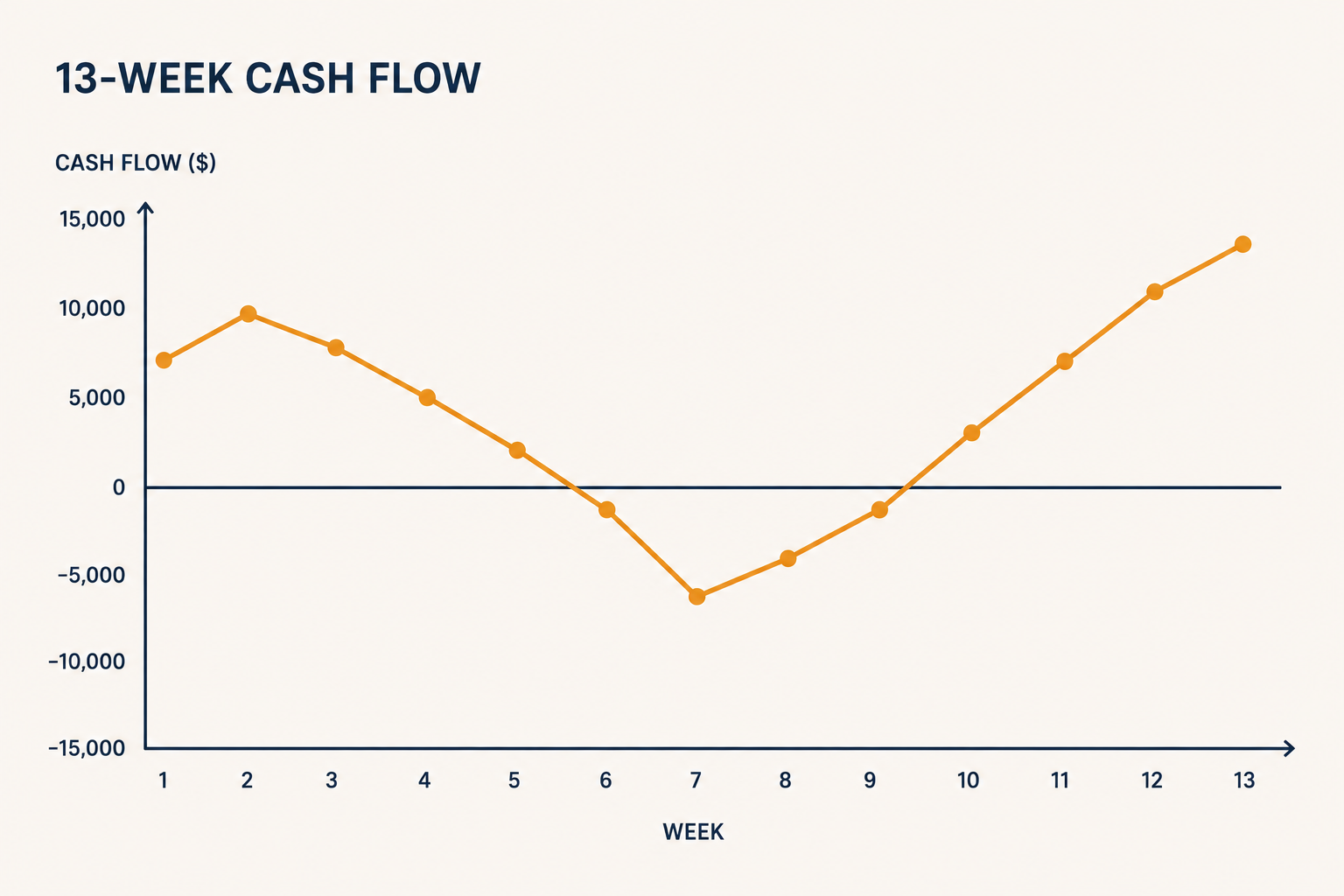

The 13-week rolling cash flow forecast

The 13-week cash flow forecast is the single most useful tool in small business finance. Simple enough to run in a spreadsheet, granular enough to spot trouble four weeks out, short enough that you’ll actually update it weekly.

The structure

A spreadsheet with 13 columns (one per week, starting this Monday) and three sections of rows: cash receipts (when money comes in), cash outflows (when money goes out), closing balance. Update every Friday for the next 13 weeks. Anything beyond that is too uncertain; anything shorter doesn’t give you time to act.

What you actually do with it

Three concrete actions, every week:

- Spot a future shortfall: if week 7 closes negative, you have six weeks to fix it. Collect overdue invoices, defer a non-essential expense, draw down a working-capital facility, delay an owner drawing.

- Time discretionary spending: new equipment, marketing investment, hiring. The forecast tells you which week has headroom.

- Track forecast accuracy: if your week-1 forecast is consistently off by 20%, your assumptions need work. Most owners overestimate customer payment speed and underestimate Friday’s BAS hit.

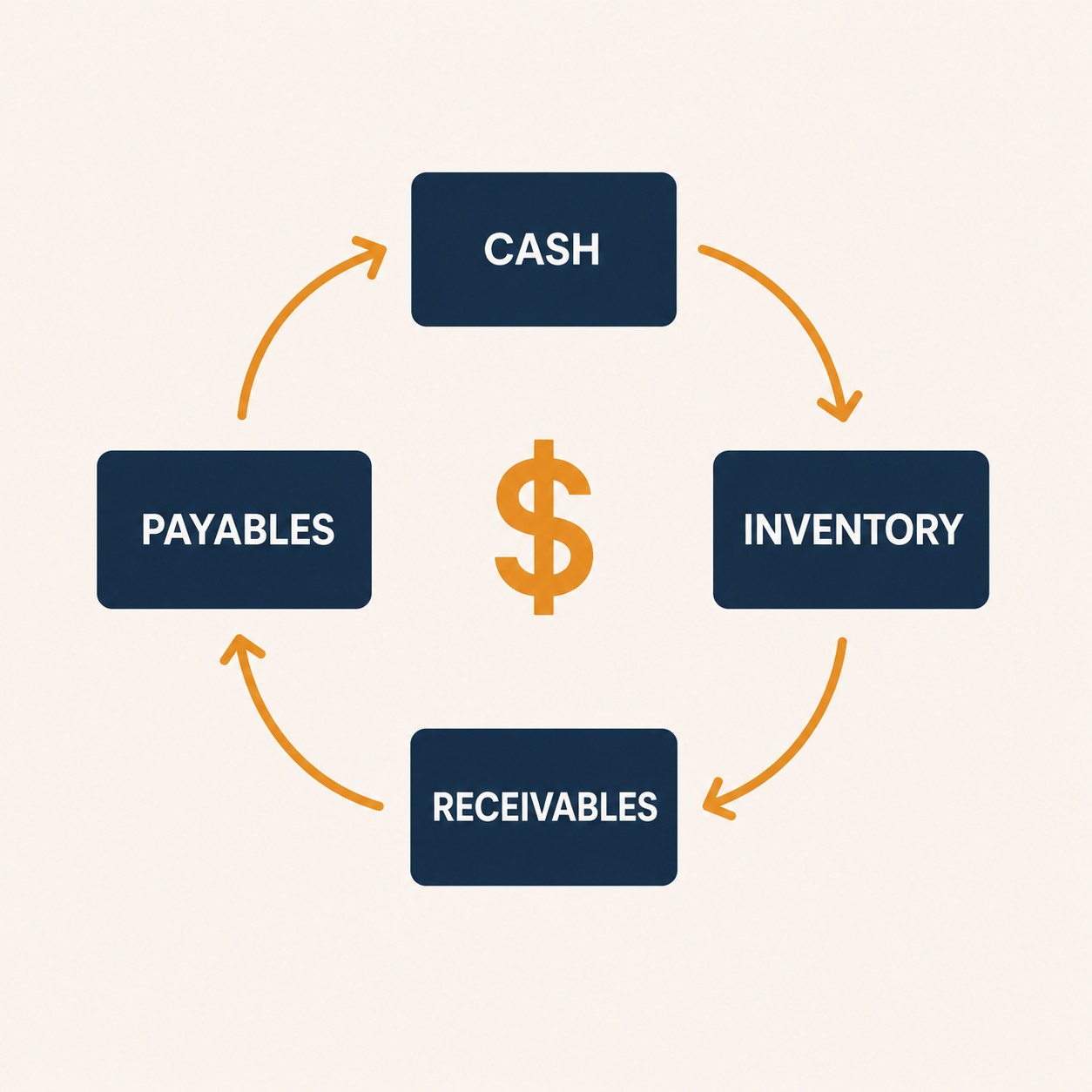

Working capital: the cycle that funds your business

Working capital is money tied up in the operating cycle – cash, accounts receivable, inventory, less accounts payable. The faster this cycle turns, the less cash your business needs.

The three levers

1. Inventory: how much stock sits on your shelves. Lower = less cash tied up = better cash flow. But too low = stockouts and lost sales.

2. Accounts receivable: how long customers take to pay. If your average customer pays in 45 days and you bring it to 30, you free up cash equal to 15 days of monthly revenue. For a $50,000/month business: $25,000 in your bank instead of theirs.

3. Accounts payable: how long you take to pay suppliers. Paying later is cash positive but stretches relationships. The art is paying late enough to manage cash without poisoning the relationships you need.

Sum of these levers is your cash conversion cycle: days inventory + days receivable − days payable. A business with a 60-day cycle needs roughly two months of operating cash on hand. A 15-day cycle needs two weeks.

The invoice discipline

Most Australian SMEs lose more cash to slow invoicing than to almost any other inefficiency.

Invoice the day work finishes, not at month-end

If you complete a job on the 3rd and invoice on the 30th, you’ve added 27 days for no good reason. Invoice the same day or next day.

Set payment terms to 14 days, not 30

Default Australian terms drifted to 30 days a decade ago and have since drifted to 45. Push back: 14 days for new customers, 7 days for completed trade jobs. Most customers pay around the same speed regardless of terms – but the terms set the trigger for follow-up.

Automate the chase

Every accounting platform has automated overdue-invoice reminders. Configure: friendly reminder day 0, firmer day 7, formal demand day 14, debt collector or final notice day 30. Don’t do this manually – you’ll skip steps and your tone will drift.

Supplier payment strategy

The objective: pay suppliers exactly when payment is due – not earlier, not later. Two practical moves:

- Set up payment runs: pay all suppliers on the same day each week (e.g., Wednesday). Concentrates outflow into predictable patterns the forecast can capture.

- Use early-payment discounts only when they’re real money: 2% net 10 vs net 30 = ~37% annualised return. Worth doing if you have the cash. Below 1% discount, usually not worth optimising at small-business scale.

The seasonal cash flow trap

Many Australian SMEs have seasonal businesses without realising it: retail (Christmas concentrates 20%+ of annual revenue into 6 weeks), hospitality (school holidays, summer), tradies (weather and pre-Christmas urgency), professional services (EOFY demand). Seasonal businesses need to plan cash flow on the calendar, not the average. The 13-week forecast plus a 12-month annual cash projection lets you see both immediate trouble and long-cycle patterns.

Building a cash buffer

Rule of thumb: every Australian SME should have 8 weeks of operating expenses in a separate account, untouched, as a buffer. Enough to absorb a major client loss, regulatory delay, or sick founder.

For a $50,000/month operating expense business, that’s $100,000 of buffer. Sounds like a lot – and it is – but it separates resilient businesses from fragile ones. Open a separate high-interest business account. Each month, transfer 5-10% of revenue automatically. Don’t touch it. Build it over 12-18 months.

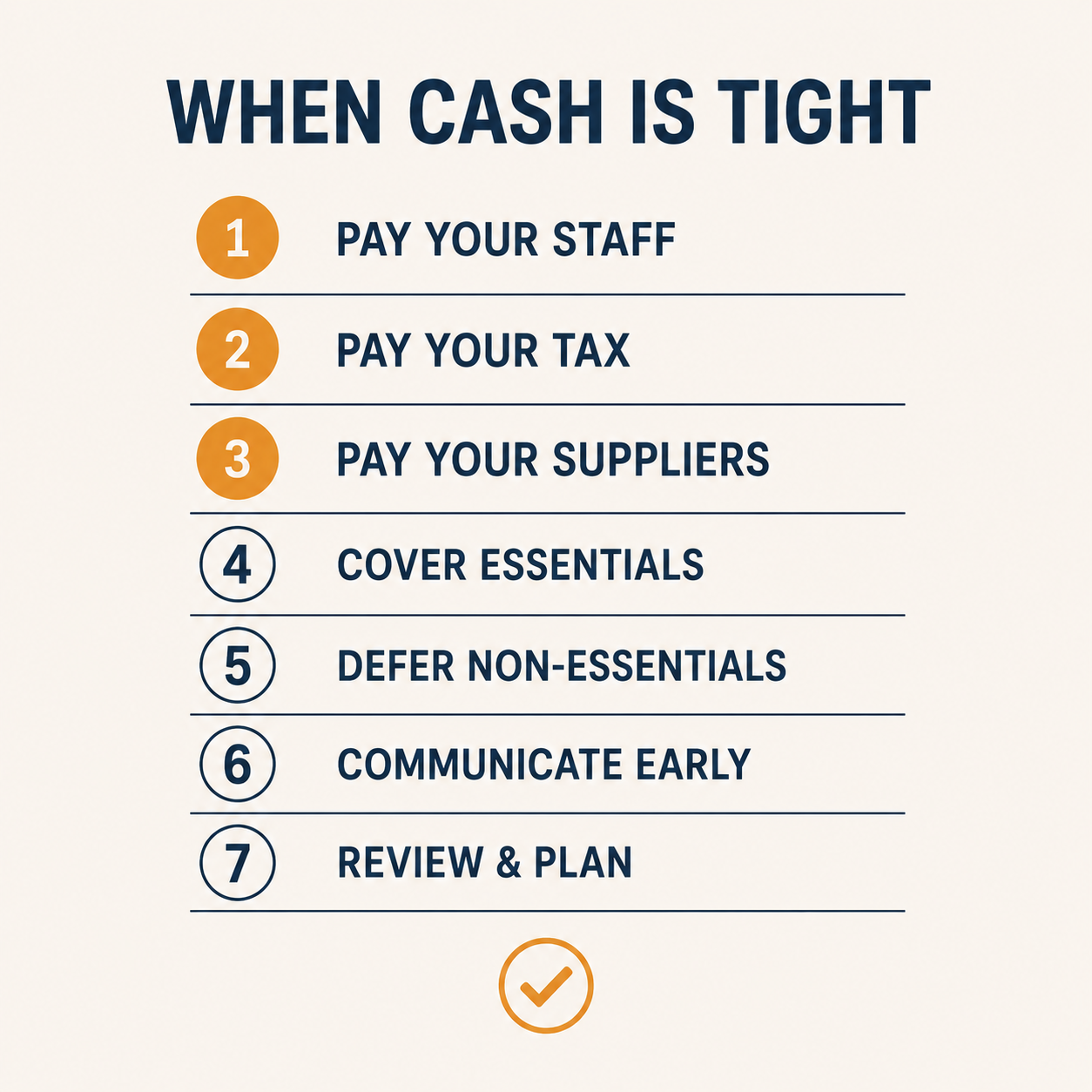

When cash is tight: the immediate moves

If you’re already in the squeeze, in priority order:

- Call your tax agent and get current – back-tax debts compound fastest, ATO has the most enforcement tools

- Call overdue customers – every 30+ day invoice gets a personal call this week

- Talk to suppliers about payment plans – they’d rather negotiate than write off

- Cut subscriptions and tools you can live without – every SME has $200-$1,000/month in unused subscriptions

- Defer owner drawings if you can

- Talk to your bank about an overdraft or temporary facility – banks lend to businesses addressing problems, not pretending

- Consider invoice financing as bridge financing, not long-term reliance

What you don’t do: ignore it. Cash crunches compound. Every week you don’t act, the options shrink.

Plain-English Australian business insights in your inbox each week

For SMEs, tradies, and founders. Free, forever.

Frequently asked questions

What’s a good cash conversion cycle?

Depends on industry. Manufacturing: 60-90 days. Retail with inventory: 30-60 days. Services without inventory: 15-30 days. Faster than industry average = strong working capital position.

Do I need a CFO?

For Australian SMEs under $5M revenue, no. You need a good accountant, modern accounting software, and the discipline to update a cash flow forecast yourself. Over $5M, a part-time CFO becomes worth the cost.

Is invoice financing a good idea?

Sometimes. Cost-of-capital is high (1-3% per month on outstanding receivables), but if it bridges you to a profitable opportunity, it can be worth it. Avoid as long-term cash management strategy.

How do I get customers to pay faster?

Shorter terms (14 days), automatic reminders, early-payment discounts when worth it (2% net 10), credit-card payment options despite merchant fees, follow-up calls within 3 days of due date. Biggest improvement usually comes from simply making the ask earlier.

What’s a healthy gross margin?

Industry-dependent. Trades: 35-55%. Retail: 30-50%. Services: 50-70%. SaaS: 70-90%. Below industry average, your pricing or input costs need attention.

Sources

- ASIC – Cash flow management for small business: asic.gov.au

- ABS – Australian small business statistics: abs.gov.au

- ATO – Bad debt deductions: ato.gov.au/businesses-and-organisations

- COSBOA: cosboa.org.au

Disclaimer: General educational information based on Australian small business finance principles as at May 2026. Not a substitute for advice from a registered tax agent, business advisor, or licensed financial planner.